Introduction

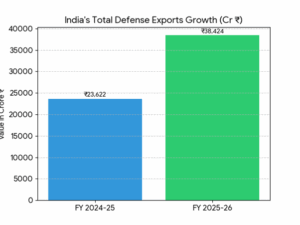

However, it was not until April 2026 that the Ministry of Defence of India released statistics that shook the world of international arms. Defence exports for the Financial Year 2025-26 touched the all-time-high mark of ₹38,424 crore ($4.6 billion), which represents an astronomical jump of 62.66 per cent compared to the preceding period. Nevertheless, the most telling part of these numbers lay within their internal distribution: whereas private defence companies enjoyed an increment of 14 per cent, their counterparts from DPSUs witnessed an export growth rate of a whopping 151 per cent. This stark difference has become a subject for heated discussions and debates within academia. Is it a new era of state-led dominance or just another “contractual peak”?

The “Peak” Argument: The Weight of Big-Ticket Contracts

The primary scepticism surrounding the sustainability of this surge stems from the nature of the products being sold. Defence exports are notoriously “lumpy.” Unlike the private sector, which often focuses on steady supply chains (components for Boeing or Lockheed Martin), DPSUs specialise in “big-ticket” platforms.

- The BrahMos and Akash Factor

A significant portion of the FY 2025–26 surge can be traced back to the delivery timelines of massive contracts signed years prior. The $375 million BrahMos deal with the Philippines and multiple batteries of the Akash Air Defence System for Armenia represent “system-level” exports.

- Concentration Risk: When a single contract (like BrahMos) accounts for a large percentage of the annual export value, the following year often sees a “dip” once the delivery phase concludes.

- G2G Dependency: DPSU exports are heavily reliant on Government-to-Government (G2G) diplomacy. While this secures large volumes, it is subject to the whims of international relations and the specific defence budgets of a few key partners like Armenia or the Philippines.

The “Sustainable Trend” Theory: A Case for Structural Shift

On the other hand, it would be a grave mistake to assume that the 151% growth is accidental rather than a consequence of the transformation process spanning over a decade within the DPSUs’ operational environment. The following are some reasons why one can argue that there is a “structural shift”:

- The Corporatisation Aspect

The corporatisation of the erstwhile OFB into seven distinct companies, such as Munitions India Limited and Advanced Weapons and Equipment India, implies an alteration in the DNA of the Indian defence industry where P&Ls come first, and export verticals are established.

Proof: As evidenced in the FY 2025–26 report, even a single entity like Munitions India Ltd won repeat contracts from Europe and the Middle East for the supply of artillery shells and explosives, indicating that while missiles can be sold, there is demand for consumable items in huge quantities.

- Diversification of the Export Portfolio

Every “peak” is characterised by the dominance of a certain product. However, in the case at hand, there is a wide variety of platforms being exported:

- HAL: The export of Dornier-228 and the worldwide promotion of Tejas Mk1A.

- BEL: Large-scale export of coastal Significant exports of coastal surveillance radars and electronic warfare suites.

- Mazagon Dock & GRSE: Increasing interest from African and South American nations in indigenous offshore patrol vessels (OPVs)

- Service & Support – The Long Tail

Sustainability in terms of defence is not only about selling but also about Maintenance, Repair & Overhauling (MRO). Through the export of platforms like BrahMos, Akash, Pinaka, DPSUs are ensuring themselves 20-30 years of revenue from servicing their customers, which means that they will earn money even after the first sale. That is what long tails mean.

Illustrates the overall trajectory of India’s defence exports. The jump from ₹23,622 crore in FY 2024–25 to ₹38,424 crore in FY 2025–26 represents a massive 62.66% year-on-year increase. This surge is largely attributed to the delivery of complete weapon systems rather than just components.

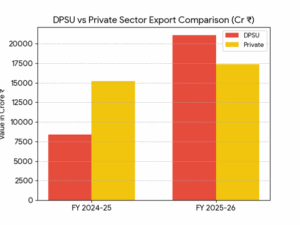

Compares the contribution of the state-owned Defence Public Sector Undertakings (DPSUs) against the Private Sector.

- FY 2024–25: The private sector was the primary driver, contributing roughly 64% of the total exports.

- FY 2025–26: The dynamic shifted significantly. With the execution of massive G2G (Government-to-Government) contracts for platforms like the BrahMos and Akash missiles, the DPSUs nearly tripled their export value, overtaking the private sector in total volume for the first time in recent years.

Role of Policy: Establishing “FLOOR” for Growth

The target set by the government is to make ₹50,000 crore worth of annual exports in the year 2029. To prevent a possible crash in the current upsurge, the following “floors” of policy have been set:

Standard Operating Procedures (SOPs): Through digitalisation of export authorisation, time for approvals has come down considerably, enabling the DPSUs to react quickly to international tender notices.

Export Financing: Through use of Lines of Credits (LoC) for the purchase of defence hardware, developing countries such as those in Africa and Southeast Asia have found themselves purchasing Indian hardware, thus establishing a constant order stream.

Indigenous Content: Since indigenous content in India is high (above 65-70%), as export increases, so do profits, which remain back in the system, helping R&D activities.

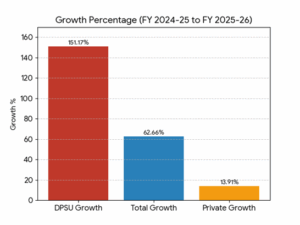

Emphasises the “Divergence” discussed earlier. By sorting the growth rates, we can see:

- DPSU Growth (151%): An exponential rise driven by the transition from ordnance factories to corporate entities and the global demand for Indian strategic platforms.

- Total Export Growth (62.66%): The healthy national average.

- Private Sector Growth (14%): A steady, linear growth that reflects a maturing supply chain and consistent participation in the global OEM (Original Equipment Manufacturer) network.

Comparing the Two Engines of Growth

| Feature | Private Sector (14% Growth) | DPSUs (151% Growth) |

| Nature of Growth | Linear & Broad-based | Exponential & Concentrated |

| Primary Export | Components, Drones, Software | Platforms, Missiles, Heavy Arms |

| Global Role | Tier 2/3 Supply Chain Partner | Primary OEM (Original Equipment Manufacturer) |

| Sustainability | High (Repeat yearly orders) | Medium-High (Cyclical but long-term MRO) |

Challenges to Sustainability

To maintain a 150%+ growth rate is impossible, but to keep the export value above ₹35,000 crore, India must address:

Competition: As Russia’s market share shifts due to the Ukraine conflict, India faces stiff competition from South Korea and Turkey, which also offer high-tech, low-cost alternatives.

Supply Chain Bottlenecks: For DPSUs to deliver on their massive order books, they must integrate more private MSMEs as subcontractors. The 14% growth in the private sector needs to accelerate to support the DPSUs’ platform-level exports.

Conclusion: A New Baseline, Not Just a Peak

While the sheer percentage jump in FY 2025–26 was undoubtedly boosted by specific large-scale deliveries to Armenia and the Philippines, labelling it a mere “peak” ignores the underlying industrial maturity.

India has moved from being a “boutique exporter” of spare parts to a “strategic partner” providing national security solutions. The surge indicates that the “Global Acceptance” of Indian tech has crossed a critical threshold. We may see the growth percentage normalise in FY 2026–27, but the floor has been permanently raised. India is no longer just participating in the global arms trade; it is beginning to shape it.

Based on the provided document and relevant academic and institutional context, the following references are formatted in APA 7 style. These sources support the data on India’s defence export trajectory, the role of DPSUs, and the strategic deals mentioned (such as BrahMos and Akash).

References

- Business Standard. (2025, April 2). Defence exports hit record Rs 23,622 cr in FY25, but pace. Business Standard. https://www.business-standard.com

- Dey, R., & Gawande, V. (2026). Analysing India’s defence export trajectory (2014–2025) through the lens of policy, industrial capacity, and geopolitical realignment. International Journal of Economic Social Science and Management Law, 7(1), 607–620.

- India Brand Equity Foundation (IBEF). (2025). India’s defence manufacturing industry. https://www.ibef.org

- International Journal of Social Sciences Bulletin. (2025). India’s export of conventional weapons to conflict zones: Ethical and strategic implications. International Journal of Social Sciences Bulletin, 1(1).

- Ministry of Defence (MoD). (2024). Aatmanirbharta in defence: MoD notifies fifth positive indigenisation list. Government of India.

- Ministry of Defence (MoD). (2025, April). Defence exports surge to a record high of Rs 23,622 crore. Government of India.

- PL Capital. (2026, February 20). India strategy: Overweight on capital goods and defense. https://plindia.com/ResReport/IndiaStrategy-20-2-26-PL.pdf

- Press Information Bureau (PIB). (2025, April). Defence exports: Annual data FY 2024–25. Government of India.

- Saxena, A. (2026, March). European rearmament: Precursors, policies, and possibilities for India (Takshashila Discussion Document 2025-06). The Takshashila Institution. https://takshashila.org.in

- Ministry of Defence. (2026). Annual Report 2025-2026. Government of India.

- Department of Defence Production. (2026). Standard Operating Procedures for export of military stores (Digitalization Edition). Ministry of Defence.

- Munitions India Limited (MIL). (2026). Operational review: Export performance in European and Middle Eastern markets.

- BrahMos Aerospace. (2024). BrahMos missile system: Global reach and export milestones.

- Bharat Electronics Limited (BEL). (2026). Investor presentation: Growth in coastal surveillance and EW exports.

- Hindustan Aeronautics Limited (HAL). (2026). Global promotion of Tejas Mk1A and Dornier-228 platforms.

- NITI Aayog. (2026, February). Scenarios towards Viksit Bharat: Sectoral insights. https://www.niti.gov.in

- Government of India. (2020). Defence Acquisition Procedure (DAP) 2020. Ministry of Defence.

By Leena, Researcher , SwadeshinShodh Sansthan